PHOTO: Finder RBNZ Official Cash Rate Survey

Property has been hailed by experts as the best investment option in the current climate according to Finder, a financial comparison site recently launched in New Zealand.

In the latest Finder RBNZ Official Cash Rate Survey, 13 experts and economists weighed in on future official cash rate (OCR) moves and other issues related to the state of New Zealand’s economy.

All experts surveyed (13/13) predict the OCR to hold at 0.25% in August, with no further movements expected this year. However, more than half (54%, 6/13) foresee further cuts in 2021, with a negative OCR not ruled out.

According to Infometrics economist, Brad Olsen, “the OCR remains on hold until retail banks have the systems in place to cope with a negative cash rate.”

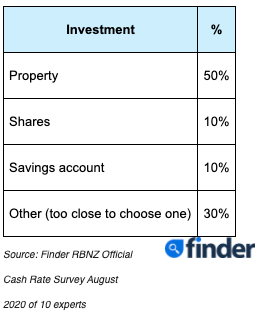

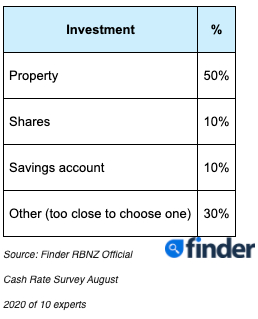

Despite reaching a historic high of $2,000 on the global equities market in early August, no experts who weighed in on the best place to invest (0/10) picked gold exclusively.

Instead, property took out the top spot, with 50% of respondents who weighed into the question (5/10) citing real-estate as the best investment option in the current climate.

Where do you think is the best place to invest your money right now?

Yet 30% of experts who weighed in (3/10) were unable to pick a single top investment, citing a mixture of shares, property and gold as the best option.

Although the nation has largely avoided the worst of a pandemic-induced downturn so far, experts have warned that the property market is not out of the proverbial woods.

Kevin McHugh, Finder’s publisher in New Zealand, said that further “tests” or hurdles are still on the horizon.

“New Zealand’s property market experienced a strong bounce-back post lockdown. Buyer confidence remained high, and a lack of property listings pushed up prices despite speculation of a slump.

“But the market will be tested during the September triple-whammy of wage subsidies ending, mortgage holidays winding down and a federal election.

“Property listings also tend to increase over spring, so we’ll need to wait and see if demand will continue to meet this additional supply,” he said.

Loan deferral scheme should be extended, experts say

As of 1 July 2020, approximately 140,000 Kiwis had either deferred or reduced their mortgage repayments.

The majority of experts surveyed (69%, 9/13) believe the government’s 6-month home loan deferral scheme should be extended past September.

Brad Olsen said the payment should continue in line with rising unemployment levels.

“With the wage subsidy extension ending at around the same time, it makes sense to extend the mortgage holiday scheme until at least the end of the year at this stage to cater for the additional job losses expected,” he said.

Ed McKnight, Economist at OPES Partners, says the market should remain stable given the low number of applicants.

“With property values holding up, I don’t see a financial stability reason for not extending the scheme, so long as the limited number of people who undertake these deferrals understand the risks and outcomes of the decision.”

Yet Michael Redell, Economist at Croaking Cassandra, disagrees with the government’s blanket approach to payment deferrals.

“Individual circumstances are best dealt with by banks on a case by case basis. While property prices hold up, banks are likely to be fairly accommodative to most. More generally, further cuts to the OCR would ease servicing burdens and should be a priority,” he said.

Here’s what our experts had to say:

Edward McKnight, OPES Partners: The commentary coming from the Reserve Bank continues to emphasise the possibility of a negative OCR. This is to allow banks to prepare for this possibility.

Brad Olsen, Infometrics: At present, the OCR remains on hold until retail banks have the systems in place to cope with a zero OCR. We also expect the Reserve Bank will hold their LSAP Programme at its current level given better than expected recent data, but reiterate its ability to expand the Programme swiftly if the economic outlook starts to show a shift to a weaker footing.

Jarrod Kerr, Kiwibank: LSAP program is the monetary policy tool of choice for now

Robin Clements, UBS NZ Ltd: There is a risk that the OCR goes lower sometime early next year, otherwise a normalisation higher is a long way off.

Alfred Guender, University of Canterbury: RBNZ is likely to hold its firepower just like central banks elsewhere. Hence a further cut in the OCR (into negative territory) at this stage would be a surprise. RBNZ is instead likely to reaffirm its commitment to using other (previously announced) unconventional monetary policy measures if necessary.

Leonie Freeman, Property Council New Zealand: I think it will remain the same in the next decision point.

Bindi Norwell, REINZ: There is a high degree of uncertainty over how various market factors will influence economic outcomes over the coming year which means it is hard to predict when the cash rate will change.

Dr Oliver Hartwich, The New Zealand Initiative: The COVID-19 outbreak in Victoria has the potential to derail the Australian economy, which appeared in recovery mode before. A severe economic and financial crisis in Australia would have a massive negative impact on New Zealand. The next step for the RBNZ’s cash rate will be down but we cannot predict the timing with any certainty.

Debbie Roberts, Property Apprentice: Latest data has shown a stronger economy than people expected post-COVID, however I don’t see pressure on the RBNZ to increase the OCR yet. I think they will keep the OCR low until mid-2021 to maintain a stimulus in the economy.

Ashley Church, ashleychurch.com: Economic signals are currently mixed and the Reserve Bank won’t want to use its firepower prematurely – however, the end of Government support after the election will likely lead to a downturn that the Bank will have no choice but to address either late this year or early next year.

Donal Curtin, Economics New Zealand: Previous commitment of RBNZ to hold rate until then

Kelvin Davidson, CoreLogic: I’m not sure that the cash rate will move in either direction for a while yet. It still seems more likely to me that looser monetary policy will take the form of more QE rather than changes to interest rates.

Michael Reddell, Croaking Cassandra: Economic/inflation outlook will continue to worsen, and the self-imposed floor on the OCR is in place until March 21.