PHOTO: First Home Buyers. FILE

| The move by the Reserve Bank to reduce the share (from 20% to 10%) of owner-occupiers that can get a mortgage with less than a 20% deposit will hit first home buyers (FHB) pretty hard – they’ve been the ones taking the most advantage of the current rules. For example, the ‘average’ FHB in Auckland may now need to find an extra $90,000 to get their deposit up to the new required level (from 1st October officially, but sooner than that if the banks move early). One consequence is likely to be a renewed focus on new-builds from FHBs, as these properties are exempt from the deposit rules. |

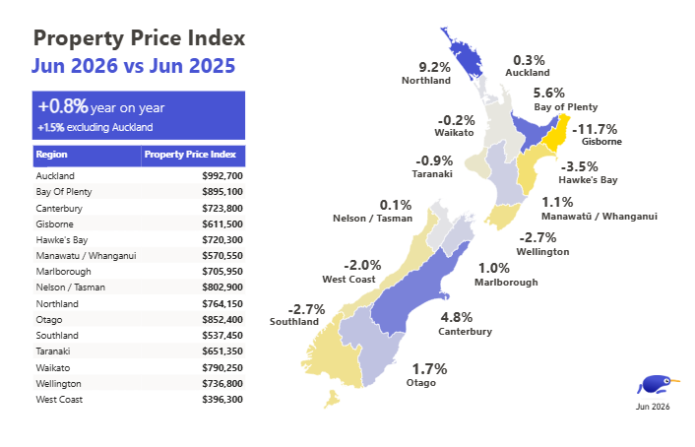

Amidst the broader surge in property values over the past year or so, first home buyers (FHBs) have obviously found themselves also having to pay significantly higher prices to get their foot on the ladder. For example, in June FHBs paid a median price of $685,275 across NZ as a whole, about $150,000 more than the figure of $535,000 in June last year. Of course, this trend of rising FHB prices paid has been in play for a while now, but has accelerated markedly post-COVID. In turn, that obviously also means an ever-increasing deposit hurdle, which some have been getting past by entering with less than the standard figure of 20%. Indeed, more than three-quarters of all owner-occupier lending done outside the 20% deposit speed limit went to FHBs in June, a figure that has steadily risen over time. Put another way, 38% of all FHB lending in June was done with less than a 20% deposit. This exemption or speed limit has been a key support for FHB demand in the property market. READ THE FULL CORELOGIC REPORT HERE: CL NZ Pulse FHBs LVRs |

MOST POPULAR

Bleak future for unvaccinated real estate agents | AUSTRALIA

Bleak future for unvaccinated real estate agents | AUSTRALIA- Abandoned land for sale

- Real estate agent in hospital after riding accident

- Real life Monopoly man reveals how he got 39 homes

- Top Auckland real estate agent – gets name suppression

- WARNING: NZ mortgage rates to RISE and put massive pressure on new first home owners

- How to be a successful real estate agent (even if you’re starting out) | WATCH

- Don Ha | New Zealand’s very own Property Guru (EXCLUSIVE INTERVIEW – PODCAST)

- The Block NZ houses are NOW for sale

- ‘We were conned’: Property management company | WATCH