PHOTO: The average New Zealand home is now worth $906,443.

For years, people talked about “The New Zealand property market“ as though every region moved together.

That is no longer the case.

The latest QV House Price Index paints a very different picture—one where some parts of the country are quietly gaining momentum while others continue to tread water or drift backwards.

The result is what may be the most fragmented housing market New Zealand has seen in years.

House Prices Remain Well Below Their Peak

Nationally, residential property values declined 0.4% over the three months to the end of June, reversing the modest gains recorded earlier this year.

The average New Zealand home is now worth $906,443, virtually unchanged from the beginning of 2026 and still 14.8% below the market peak reached in 2022.

While these national figures appear relatively stable, they hide dramatically different stories playing out across the country.

A Property Market of Winners and Losers

Rather than moving in unison, regional markets are increasingly following their own paths.

According to QV, Christchurch, Canterbury and Southland continue to outperform, while Auckland and Wellington remain subdued.

QV spokesperson Simon Petersen says the national average masks a growing regional divide.

That divide is becoming more pronounced with every quarterly update.

Canterbury Continues to Shine

If there is one clear standout in New Zealand’s property market, it is Canterbury.

Home values across the region increased 0.9% during the quarter, making Canterbury one of the country’s strongest-performing regions.

Every district recorded average value growth.

Christchurch itself rose 0.9%, lifting the city’s average home value to $805,736.

Even more impressive, Christchurch values are now 3.9% higher than a year ago.

Why Christchurch Keeps Winning

Several factors continue driving Christchurch’s resilience.

These include:

- Relative affordability

- Strong internal migration

- Modern housing stock

- Balanced supply and demand

- Active first-home buyer market

- Continued investor interest

- Ongoing infrastructure investment

Premium suburbs such as Merivale, St Albans and Papanui continue attracting strong demand, while townhouse buyers remain active thanks to recent price corrections.

For many buyers priced out of Auckland, Christchurch is increasingly being viewed as one of New Zealand’s best value major cities.

Southland Continues to Surprise

Quietly, Southland has become New Zealand’s strongest-performing region.

Property values increased 1% during the quarter.

Highlights include:

- Gore +5.4%

- Invercargill +1.5%

These gains continue a trend that has seen Southland outperform much larger centres over recent years.

Lower entry prices, strong rental demand and attractive yields continue drawing investor attention south.

Auckland Still Searching for Momentum

New Zealand’s largest housing market remains subdued.

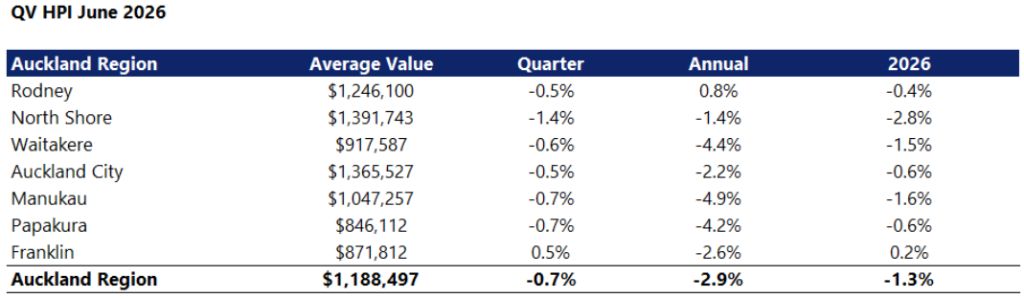

Auckland home values declined 0.7% over the quarter, with the average property now valued at $1,188,497.

Values are:

- 2.9% lower than a year ago

- 1.3% below the start of 2026

Only Franklin recorded quarterly growth, while Rodney remains the only former council area with annual gains.

Buyers Hold the Power

According to local valuers, Auckland buyers continue to enjoy favourable conditions.

There is:

- Plenty of housing stock.

- Strong competition among sellers.

- Greater willingness to negotiate.

- More low offers being accepted.

First-home buyers remain active, particularly in the townhouse market, but urgency is largely absent.

Today’s buyers know they have options.

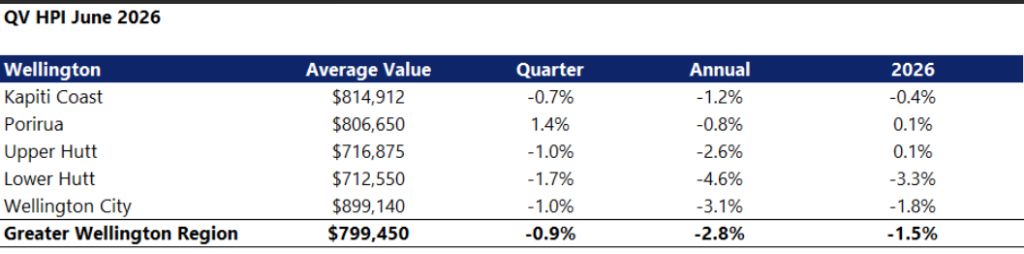

Wellington Faces Ongoing Challenges

The capital continues struggling.

Most parts of Wellington recorded declining property values during the latest quarter.

Only Porirua managed modest growth.

QV attributes much of the weakness to:

- High housing supply.

- Economic uncertainty.

- Public sector job cuts.

- Higher interest rate expectations.

- Reduced buyer confidence.

These factors continue weighing heavily on demand.

Waikato Remains Steady

Hamilton and the wider Waikato region remain relatively stable rather than spectacular.

Hamilton recorded a 0.6% decline during the quarter.

Despite softer values, first-home buyers continue supporting activity while investors remain cautious as they watch interest rate movements.

Bay of Plenty Delivers Mixed Results

The Bay of Plenty continues living up to QV’s description of a patchwork market.

Positive performers included:

- Tauranga +0.9%

- Whakatāne +0.4%

Meanwhile several districts experienced noticeable declines.

This highlights just how localised New Zealand’s property market has become.

First-Home Buyers Keep the Market Moving

One encouraging trend remains consistent nationwide.

First-home buyers continue purchasing.

Higher stock levels have given buyers:

- More choice.

- Greater negotiating power.

- More time for due diligence.

Unlike the frantic market of 2021, today’s buyers are carefully comparing properties rather than rushing to secure them.

Interest Rates Still Cast a Shadow

Much of the market’s direction now depends on interest rates.

QV notes that today’s Official Cash Rate announcement—and any future moves by the Reserve Bank—will play an important role in shaping buyer confidence during the second half of 2026.

Higher borrowing costs generally reduce affordability and slow market momentum.

Conversely, any future easing in monetary policy could help stimulate demand.

What Does This Mean for Investors?

For investors, blanket national strategies are becoming increasingly risky.

Instead, success is likely to depend on choosing the right region.

Current trends suggest stronger opportunities may exist in markets offering:

- Better affordability.

- Population growth.

- Healthy employment.

- Balanced housing supply.

That partly explains why Canterbury and Southland continue outperforming larger centres.

The Bottom Line

The days of New Zealand’s housing market moving together appear to be over.

Instead, regional differences are becoming more important than ever.

While Auckland and Wellington continue facing affordability pressures, economic uncertainty and abundant housing stock, Christchurch, Canterbury and Southland are quietly building momentum.

For buyers, sellers and investors alike, understanding local market conditions has never been more important.

One thing is becoming increasingly clear:

There isn’t one New Zealand property market anymore. There are dozens of local markets—each writing its own story.

Frequently Asked Questions

Which region is performing best?

According to the latest QV House Price Index, Southland recorded the strongest quarterly regional growth, with Canterbury close behind.

Which major city is performing best?

Among New Zealand’s largest cities, Christchurch continued to outperform Auckland and Wellington during the June quarter.

Are house prices still falling?

Nationally, average residential values eased 0.4% over the latest three months, although performance varies significantly by region.